|

January 27, 2026

|

2:18 PM

|

January 27, 2026

|

2:18 PM

-3.jpg?width=628&height=314&name=Blog%20headers%20%232%20(4)-3.jpg)

Last week, the world’s biggest opportunities (and challenges) were compressed into a few square miles of Swiss mountain real estate – along with CEOs, officials, investors, and assorted leaders in sensible shoes trying to make sense of it all. I was able to navigate it all without slipping on any ice, which I consider my biggest professional victory of the week.

Davos is part policy summit, part investor meeting, and part group therapy for global systems under stress. This year felt different from recent editions, somehow less theatrical and more forensic. I saw fewer slogans but more spreadsheets.

As one CEO shared with me about their company’s goals for the week, “We’re not here debating ideals. We’re comparing insurance deductibles and cost of capital. Markets are learning how to price fragility.”

That single sentence framed the entire week.

Across industries and continents, six themes kept resurfacing—on stage, in private meetings, and in the late-night conversations where far more honesty tends to surface.

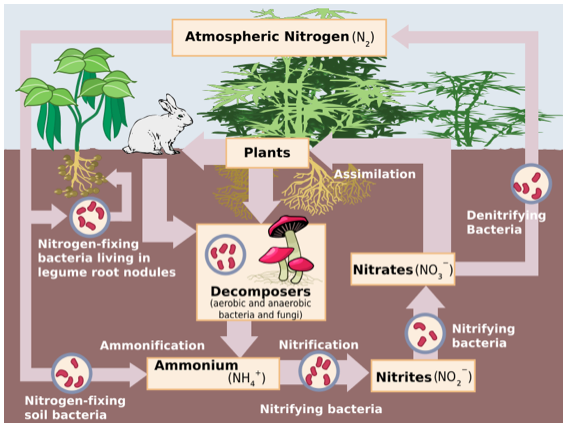

1. Water is becoming a strategic asset (and it’s beginning to be priced)

Water security has crossed the line from an “environmental issue” to a “board-level risk” for many companies and most nations.

It surfaced in conversations about semiconductors, food inflation, data centers, insurance pricing, and sovereign stability. Capital is quietly becoming more expensive for water-stressed regions, companies, and projects. Insurance is retreating in some places. Credit committees are asking hydrology questions.

Water is becoming a balance-sheet variable, not merely an operating constraint.

I get to see this weekly at Holganix in grower dashboards, not as theory. Fields with depleted biology shed water like pavement and suffer runoff after short rains, crop stress after long ones, and expensive inputs wash away. Fields with healthy soil hold water and nutrients like a savings account.

Healthy soil doesn’t just grow crops. It stores water like capital.

When soil goes into water bankruptcy, everything downstream—literally and financially—follows. Sophisticated operators and investors are already acting on this.

2. “Sustainability” put on a suit and joined the risk committee

The S-word—a four-letter word to some today—certainly appeared on fewer badges and panel titles than in years past, but it hadn’t disappeared.

It had matured.

Executives spoke less about targets and more about continuity, insurability, weather exposure, and what nature is doing to their cost of capital. When lenders widen spreads and insurers walk away, philosophy turns into math.

Several executives noted that the center of gravity is shifting from reporting impacts to engineering around them. Carbon, water, and land constraints are no longer handled by ESG teams after the fact; they are showing up upstream in plant location decisions, supplier selection, product architecture, and long-term capital planning.

Nature-related risk is following the same arc cyber risk did: first ignored, then modeled, eventually priced, and now unavoidable.

Data is driving much of this evolution. Now that these impacts can be measured—along with their financial consequences—bankable transitions are becoming more common than public commitments. Banks, insurers, private equity firms, and sovereign funds are embedding water stress, soil degradation, energy reliability, and political volatility directly into underwriting and valuation models.

My finance friends discuss volatility the way my farmer friends talk about weather: inevitable, inconvenient, and obviously someone else’s fault.

Volatility is no longer the exception. It’s the business model.

3. Soil is being recognized as financial infrastructure

This one felt personal—and, of course, a little self-serving.

Across sessions on food security, climate adaptation, economic development, global water impact, and more, soil kept reappearing—not as dirt to expense annually, but as a productive system to capitalize.

Agricultural land has been treated like a rental car far too often, with similar depreciating results. We are entering a time when growers, bankers, companies, and countries will see soil as a factory-like asset—a system that requires investment, maintenance, and disciplined management to keep producing:

- a yield stabilizer

- a water regulator

- a carbon storage system

- a rural economic engine

- a volatility buffer

- an input-efficiency indicator

If roads move goods and fiber moves data, soil moves food, water, carbon, and stability. Neglect it, and you don’t just lose crops. You lose optionality.

Growers, companies, and countries can neglect soil health season after season (many always have). Data is now showing that those who do pay a price for that choice that spans decades.

.jpeg?width=400&height=300&name=Image%20(11).jpeg)

Tim during a panel at Newsweek speaking on “Higher Yields, Lower Impact: Farming for More with Less”.

4. Agriculture, for better and worse, at the forefront of geopolitics

Food systems used to sit politely in the background of global strategy.

Not anymore.

At Davos, agriculture was discussed the way energy has been in the past: as national security infrastructure. Tariffs. Export controls. Fertilizer supply chains. Diesel costs. Sanctions. Climate migration. Strategic grain reserves. For multinational companies, this means sourcing, investment, and market entry are becoming political decisions, not just economic ones.

Efficiency now has to include resilience. Optimization must address redundancy. Cheapest is giving way to what is most reliable.

Two deeper shifts are underway.

First, data and biology are becoming strategic assets. Seed genetics, soil data, yield models, and biological inputs are now discussed in the same terms as rare earths and energy reserves. Who controls the data layer of food production—and who owns the underlying biology—will shape trade leverage in the way ports or pipelines do.

Agriculture is becoming geopolitical leverage.

Second, food security is quietly reshaping alliances. Several conversations hinted that future trade blocs may form less around ideology and more around protein, calories, water, and fertilizer access. Nations with reliable surplus production and resilient soils will carry disproportionate diplomatic influence. Those without it will face constraints no amount of monetary policy can solve.

The next decade of agriculture will be shaped as much by diplomacy as by agronomy.

5. Carbon is ready for a financial-markets methodology

For years, carbon markets were built like academic projects: scientifically rigorous, carefully bounded, and structurally small. That made them credible. It did not make them functional at scale.

What I heard shifting in Davos was not enthusiasm, but intent.

Executives, financiers, and policymakers spoke about carbon less as a moral instrument and more as a missing piece of market plumbing—something that needs liquidity, standards, risk models, contract structures, clearing mechanisms, and price discovery.

Several global market makers described how financial methodologies are being redesigned to accommodate institutional capital, long-duration offtake agreements, and sovereign participation. One leader put it plainly: “The drought of market creativity in carbon is ending.”

Carbon is being pulled into the same framework as energy, metals, and agriculture—not because it is fashionable, but because companies and countries now need it to manage three converging pressures:

- regulatory compliance

- supply-chain resilience

- land and water security

Soil-based sequestration sits at the intersection of all three, which explains why it kept surfacing not only in climate sessions, but also in conversations about food security, trade exposure, and national planning.

The voluntary phase is ending, and with the growing depth of data to drive it, the infrastructure phase has begun. What follows is less romantic, but far more consequential: pricing models, counterparty risk, insurance treatment, accounting standards, and integration into procurement strategies.

One investor joked they will soon be recruiting soil scientists the way they once recruited software engineers. I don’t think they were joking.

The quiet opportunity learned from the very loud party

For all the talk of risk, Davos wasn’t pessimistic.

It was, however, pragmatic.

It was meaningful and fascinating to sit with leaders who have spent decades navigating booms and crises, bubbles and resets. By the end of the week, most shared the same posture: bullish on resilience, bearish on sleep.

The common thread wasn’t climate. Or technology. Or geopolitics.

It was that resilience is being redefined as a financial strategy.

The next generation of winning companies and nations will be the ones that:

- treat natural systems as productive long-term assets, not annualized expenses

- actively design for volatility advantage instead of assuming passive stability at the supply-chain, corporate, and national levels

- understand that soil, water, data, and trust will compete on reliability as much as they will on price

Not because any of this sounds virtuous.

Rather, because it pencils.

At Holganix, we see clearly this convergence of soil, data, water, and finance daily. Davos simply confirmed that it’s now global.

Until next year, Davos!

-1.jpg)

.jpg)

.jpg)

.jpg)

-1.png)

-2.jpg)

-1%20(1).webp)

-831535-2.webp)

- blog (419)

- lawn care (374)

- agriculture (220)

- golf course (202)

- sports turf (199)

- holganix reviews (167)

- story (131)

- Holganix Bio 800 (32)

- farmers (30)

- soil health (28)

- soil (17)

- Holganix Bio 800+ Revive (16)

- trees (16)

- webinar (16)

- holganix case studies (15)

- Holganix Bio 800 Breakdown (14)

- Soil heath (12)

- Holganix Bio 800 Agriculture (11)

- soil microbes (10)

- carbon (9)

- HGX (8)

- crop residue (8)

- holganix results (8)

- fertilizer (7)

- Gratitude (6)

Related Posts

-1.png)

-1.png)